When Shoppers Stop: What April's Spending Collapse Means for Mid-Market UK Retail

The first annual fall in consumer spending since November 2024 wasn't a blip. It was a warning shot -- and most retailers are still pointing their guns at the wrong target.

British consumers spent less in April 2026 than they did a year ago. That sentence sounds simple, but the mechanics underneath it are anything but. This wasn't just Easter timing. This wasn't just one bad month. This was the moment the Iran war arrived on the UK high street -- and the question for every mid-market retailer right now isn't whether this hurts. It's whether you can see clearly enough to do something useful about it before the damage compounds.

1. The Numbers That Broke the Run

For context: UK consumer card spending had been growing, slowly, for most of the past year. Even in difficult quarters, the headline figures stayed positive. That run ended in April.

| Metric | March 2026 | April 2026 | Change |

|---|---|---|---|

| Barclays card spending YoY | +0.9% | -0.1% | Reversal |

| BRC total retail sales YoY | +3.6% | -3.0% | -6.6 pts |

| BRC like-for-like sales YoY | +3.1% | -3.4% | -6.5 pts |

| Non-food retail sales YoY | +6.1% | -3.3% | Sharp decline |

| In-store non-food YoY | +5.6% | -4.0% | Worst in months |

| Barclays travel spend YoY | -- | -5.7% | Steepest fall |

| Essential spend (Barclays) | -- | +0.3% | Slight positive |

| Fuel card spend | -- | +10.4% | Highest since Dec 2022 |

Sources: Barclays Consumer Spending Report May 2026, BRC-KPMG Retail Sales Monitor May 2026

The BRC was careful to note that Easter falling in March this year, rather than April, distorted the month-on-month picture. If you combine March and April, total retail sales are up 1.5% year-on-year. That's technically positive. It's also below the 12-month average growth rate of 1.8%. And it's below the UK's latest CPIH inflation rate of 3.4%, which means real retail volumes are still contracting.

Here is the uncomfortable framing: even the "adjusted" figure that smooths out Easter noise is a picture of retail running slower than inflation. In real terms, UK consumers are buying less than they were a year ago. The nominal numbers have been flattering a structural retreat.

Key insight: When the "good news" read -- combining two months to offset Easter -- still lags inflation by nearly two percentage points, there is no good news. There's just slower bad news.

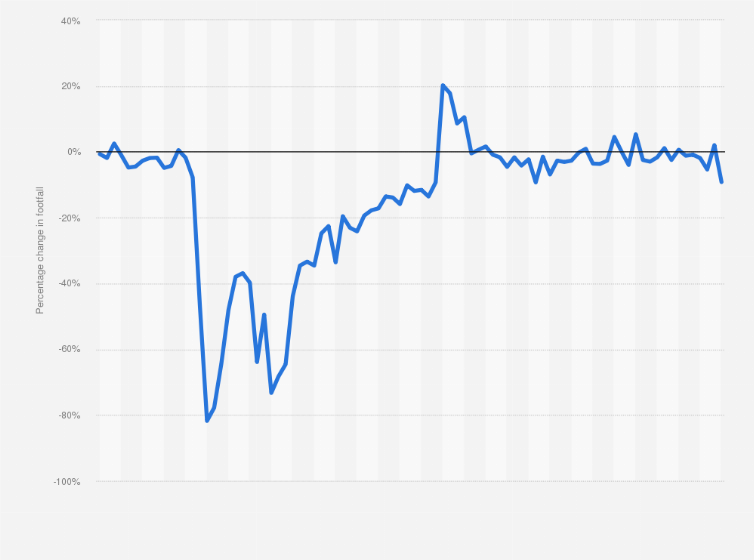

Caption: UK high street footfall came under renewed pressure in April 2026 as consumers prioritised savings over discretionary spending. Source: Wikimedia Commons

Caption: UK high street footfall came under renewed pressure in April 2026 as consumers prioritised savings over discretionary spending. Source: Wikimedia Commons

2. What Actually Happened: The Iran War and the Confidence Collapse

On 28 February 2026, the US and Israel launched strikes against Iran. Iran responded by announcing it would close the Strait of Hormuz -- a passage through which roughly one fifth of global oil and gas trade moves. Shipping through the Strait largely ceased. A ceasefire was announced on 8 April, but the Strait remains subject to a US naval counter-blockade.

The practical consequence for UK consumers came fast. UK CPI inflation climbed to 3.3% in March 2026, up from 3.0% in February. Fuel prices surged -- Barclays recorded a 10.4% annual rise in card spending on fuel in April, the sharpest increase since December 2022. Energy costs, already structurally elevated by the transition away from Russian gas after 2022, got a second shock.

But the bigger effect wasn't petrol prices. It was psychology.

PwC's quarterly consumer sentiment index, based on a survey of over 2,000 UK adults conducted after Easter, fell from -1 in January to -13 in April. That's the sharpest quarterly drop since mid-2022 -- when the Ukraine war began. Confidence is now at its lowest reading since the September 2023 recession.

| Confidence indicator | Q1 2026 | Q2 2026 | Change |

|---|---|---|---|

| PwC Consumer Sentiment Index | -1 | -13 | -12 pts |

| % concerned about cost of living | ~70% | ~89% | Significant rise |

| % saying conflict affects spending plans | -- | ~75% | -- |

| % under-45s worried about job security | -- | 63%+ | -- |

| % skilled manual workers worried about job security | -- | 50%+ | -- |

Sources: PwC Consumer Sentiment Q2 2026, BritBrief reporting

The Energy and Climate Intelligence Unit think tank warned that food costs could be 50% higher by November compared with the start of the original cost-of-living crisis in 2021, as supermarkets grapple with input costs they cannot fully absorb.

"Consumer confidence has been further dampened by rising prices due to the Iran conflict, with consumers cautious about potential ongoing effects. As a result, the retail sector is facing a challenging start to spring/summer." -- Linda Ellett, UK Head of Consumer, Retail & Leisure, KPMG, May 2026

What happened in April wasn't irrational. Consumers looked at rising energy bills, uncertain food prices, and a war with no clear end date -- and they did exactly what rational economic actors do under uncertainty: they stopped spending on things they could defer, and they put money aside.

3. The Categories That Took the Hit

Not all retail got hurt equally. And the pattern of who lost and who held tells you a lot about where this consumer retreat is coming from.

| Category | April 2026 Performance | Context |

|---|---|---|

| Travel spending (Barclays) | -5.7% YoY | Steepest fall in data |

| Hotels (Barclays) | Sharp decline | Part of travel pullback |

| Furniture & big-ticket home | Fell | Recovery from 2025 stalled |

| Non-food (in-store) | -4.0% YoY | Worst recent reading |

| Fashion & footwear | Declined | Below-average contribution |

| Health & beauty | Marginally positive | Outperformed |

| Jewellery & watches | Marginally positive | Outperformed |

| Grocery / food essentials | Easter-distorted, mixed | Still baseline demand |

| Fuel | +10.4% YoY | Forced spend, not choice |

Sources: BRC-KPMG Retail Sales Monitor, Barclays Consumer Spending Report, FashionNetwork analysis, May 2026

The BRC's online growth rankings tell a secondary story worth noting. Health and beauty rose to first place in online category performance in April, up from fifth in March. This mirrors a pattern seen during previous uncertainty periods: consumers trade down from fashion and interiors but protect their beauty and personal care routines -- especially through online channels, where price comparison is easier.

Travel was the category that took the sharpest absolute hit -- down 5.7% on Barclays card data. That's not an Easter effect. That's consumers genuinely pulling back on holiday booking and hospitality spend, likely weighing up whether a trip to regions near active conflict zones makes sense, and whether they can afford it as energy costs eat household budgets.

Furniture tells a subtler but important story. BRC data showed the recent recovery in furniture sales losing steam in April. The furniture category is a classic canary: it's expensive, it's deferrable, and it requires a degree of future confidence (you need to believe you'll still be living somewhere you want to furnish). When furniture stalls, it usually means something more structural is happening to consumer planning horizons.

Ask yourself: If your business has more than 20% of its revenue in big-ticket, deferrable, or travel-adjacent categories, are you modelling a Q2 revenue scenario that assumes continued contraction rather than recovery?

4. The Macro Picture: How Bad Could This Get?

The April data sits inside a broader economic revision that is, frankly, sobering.

Before the Iran conflict, the UK was tracking GDP growth of around 1.3% for 2026. That forecast has been revised down multiple times in under three months.

| Forecaster | GDP growth forecast (pre-conflict) | GDP growth forecast (current) | Revision |

|---|---|---|---|

| IMF | 1.3% | 0.8% | -0.5 pts (sharpest G7 revision) |

| EY | 1.3% | 0.8% | -0.5 pts |

| Treasury (independent avg.) | 0.9% | 0.6% | -0.3 pts |

| EY (downside scenario) | -- | 0.3% | If Hormuz stays closed |

Sources: IMF April 2026 WEO, EY Economic Outlook May 2026, HM Treasury survey of independent forecasts April 2026, House of Commons Library

EY chief UK economist Peter Arnold was blunt about the consumer outlook: "Cautious levels of consumer spending seen since the pandemic also now appear more structural than temporary, with all income groups reallocating household spending towards savings and essentials and away from discretionary spending." That phrase -- more structural than temporary -- should be underlined, printed, and read at every board meeting happening in UK retail right now.

What he's describing is a consumer who was already in a cautious mode before the Iran war, and who has now used an external shock to give themselves permission to extend that caution further. The war didn't create the instinct to save. It validated it.

EY's base case for UK consumer spending growth in 2026 is now 0.3%, down from 0.9% pre-conflict. If the Strait of Hormuz remains disrupted for the rest of the year, that number could fall further.

Key insight for retail leaders: You're not planning for a bad spring. You're planning for a structural shift in consumer psychology that arrived before April and won't leave when the headlines change. That's a different problem.

5. The Mid-Market Squeeze: Why This Hurts £5M-£50M Operators More Than Anyone

The macro figures get reported. The analyst takes get written. But here's the thing most retail commentary misses: the pain is not evenly distributed, and mid-market operators -- those running businesses in the £5M to £50M revenue range -- face a particularly difficult combination of forces.

Large retailers -- your Tesco, your Next, your M&S -- can absorb a bad month or two through sheer scale and balance sheet. Their buying power gives them margin protection. Their marketing budgets allow them to defend share even when the market contracts.

Value retailers -- your B&M, your Home Bargains, your Primark -- benefit from consumer trade-down. When people feel poorer, they trade to cheaper. These businesses can actually grow in a confidence crisis.

The mid-market is caught in the middle. You don't have the buying power of the big operators to hold prices down. You don't have the price positioning to capture the trade-down shopper. And your customer -- broadly speaking, a household spending £30,000 to £60,000 a year -- is exactly the demographic that feels most financially squeezed when energy bills and food costs rise. They have discretionary income to protect. They know it. And they're protecting it.

| Business Type | Position in April 2026 | Risk Level |

|---|---|---|

| Large supermarket chains | Stable (essential demand) | Low |

| Large fashion multiples (Next, M&S) | Defensive but resilient | Low-medium |

| Value/discount retailers | Potential beneficiary | Low |

| Mid-market fashion (£50-£200 AOV) | Consumer directly deferring | High |

| Mid-market home/furniture | Big-ticket freeze | Very High |

| Mid-market travel/hospitality-adjacent retail | Direct hit | Very High |

| Mid-market health & beauty | Relative outperformer | Medium |

| Mid-market specialist/gift retail | Deferrable, vulnerable | High |

The structural challenge for a mid-market operator right now is that your customers have not stopped spending in total. They've reconfigured what they're willing to spend on. Essentials and beauty are holding. Travel and big-ticket are collapsing. Fashion is somewhere in the middle, soft but not catastrophic. If your product or service sits anywhere close to "nice to have, can wait," you should be asking hard questions about your Q2 and Q3 pipeline.

Caption: Shifting UK consumer spending priorities -- categories linked to wellbeing and essentials holding as discretionary categories contract. Source: Statista

Caption: Shifting UK consumer spending priorities -- categories linked to wellbeing and essentials holding as discretionary categories contract. Source: Statista

6. Beauty Holds, But Don't Get Comfortable

The one genuine bright spot in the April data is health and beauty. The BRC's online growth rankings put health and beauty in first place -- up from fifth in March. The ONS confirmed that cosmetics and toiletries stores showed growth across all three months of Q1 2026, with retailers reporting new collection launches.

This is not a coincidence. It's a pattern. Beauty is what retail analysts call a "lipstick category" -- it tends to hold or even grow during downturns because it provides a low-cost emotional payoff. A £25 moisturiser feels like a treat when a £500 weekend away is off the table. A new mascara is a mood-lifter when a new coat isn't on the cards.

But here's the thing mid-market beauty operators need to understand: the same emotional logic that protects your category in a downturn also makes it highly competitive. When consumers do spend on beauty, they're more deliberate. They're reading reviews. They're comparing. They're buying things that feel worth it -- not things that feel fine.

The beauty retailers that are winning right now aren't just riding the category wave. They're winning on specificity: clear product stories, strong value anchoring, excellent online execution. The ones that will struggle are those that rely on the category doing the work for them.

GlobalData analyst Sofie Willmott put it plainly: "Weak consumer confidence in 2026 will hinder retail spending and while some level of uncertainty remains, shoppers are likely to focus their buying on essential products like groceries and health & beauty items." That's the good news. The challenge is that every other mid-market beauty operator just read the same line.

| Beauty sector performance signal | Status |

|---|---|

| BRC online category ranking (April) | 1st (up from 5th in March) |

| ONS cosmetics & toiletries Q1 2026 | Positive across all 3 months |

| Consumer preference in downturn | Prioritised over fashion & home |

| Competition intensity | Rising as category attracts more focus |

| Margin pressure from energy/supply costs | Increasing |

7. Fashion: The Sector Caught Between Two Fires

Fashion in April was neither the worst performer nor a story worth celebrating. Both clothing and footwear sales dipped in April, though clothing managed to climb from ninth to fifth in the BRC's online growth rankings. That's relative -- it means clothing was less bad online, not that it was doing well.

The deeper challenge facing mid-market fashion right now is that its customers are facing exactly the two-sided squeeze that hurts discretionary non-essentials most: higher essential costs (energy, food, fuel) are eroding the discretionary budget, while uncertainty about future costs is making consumers reluctant to spend even what they technically have available.

March's clothing rise -- the strongest since July 2025 according to FashionNetwork data -- had been attributed partly to better weather in February and March. Weather-driven spending tends not to persist. If spring turns unremarkable or consumers stay anchored to their savings anxiety, the temporary warmth that lifted clothing in March won't repeat.

The structural problem for mid-market fashion is also about value. A consumer who spent £80 on a dress in 2024 is now asking whether they need it, whether a cheaper version would do, and whether waiting a few weeks until a sale might make more sense. The answer to all three questions is "yes" when confidence is low. That's not a marketing problem that better Instagram ads can fix.

"April's sales fall was largely driven by the Easter shift, with food hit hardest. But weak consumer confidence also played a role as fears about the Middle East conflict driving up living costs led shoppers to rein in spending. Big-ticket purchases fell, with the recent recovery in furniture losing steam, and uncertainty around summer holidays hitting discretionary spend." -- Helen Dickinson, Chief Executive, British Retail Consortium, May 2026

8. The Savings Pivot: What Households Are Actually Doing

One of the most significant signals in the April data -- and one that's received less coverage than the headline spending decline -- is the savings behaviour underlying it.

Jack Meaning, Barclays' chief UK economist, described the April shift in precise terms: consumers are building savings buffers in direct response to the Middle East shock. This is not passive saving -- saving by accident because there's nothing to buy. This is active saving, a deliberate reallocation from spending to precautionary reserves.

This matters for mid-market retailers for a specific reason. When consumers are saving passively, a good offer or a compelling product can unlock spend. When consumers are saving actively -- because they are anxious about a specific set of future costs they cannot control -- the marketing lever is weaker. You're not up against competing retailers. You're up against the consumer's own sense that financial prudence is more important right now than anything you're selling.

The BCC's Quarterly Economic Survey described the UK economy as "operating below potential, with limited resilience to absorb further shocks." That framing applies equally to the consumer household. UK households have been shock-buffeted since 2020 -- Covid, Ukraine, cost-of-living crisis, and now the Iran conflict. The precautionary savings instinct has been trained and strengthened over six years. It doesn't switch off quickly when headlines change.

| Consumer behaviour pattern | April 2026 signal | Implication for retailers |

|---|---|---|

| Active savings building | Rising, confirmed by Barclays | Harder to unlock with promotions |

| Travel spend deferral | -5.7% YoY | Hospitality and adjacent retail hit |

| Big-ticket deferral | Furniture stalled | Capital goods and home retailers vulnerable |

| Essential spend holding | +0.3% | Grocery and health basics protected |

| Fuel forced spend | +10.4% | Compressing disposable income further |

| Online vs in-store | Online beauty up, in-store non-food -4% | Channel mix matters more now |

Ask yourself: Is your current marketing strategy built around reasons-to-buy? Because right now, the primary factor is reasons-to-wait. Those are different problems. One needs messaging. The other needs a different product, price point, or urgency construct entirely.

9. The Compounding Costs Problem: It's Not Just the Consumer

Here's a dimension of April's data that retail operators need to hold alongside the consumer story: you're not just facing a demand problem. You're facing a cost problem at the same time.

The BRC sent a warning in late April that retailers are absorbing significant additional costs from the Middle East conflict, on top of existing government-driven cost pressures already baked into 2026. The April 2026 abolition of business rate relief -- phased down from 75% to 40% in April 2025, and now removed entirely -- has added direct cost pressure to the retail P&L just as consumer demand is softening.

Plastic packaging tax changes, National Living Wage increases, higher National Insurance contributions, and rising energy bills for operational premises are all landing simultaneously on operators whose revenue line is either flat or negative in real terms.

| Cost pressure | Impact on UK retail | Status in 2026 |

|---|---|---|

| Energy price rise (Iran conflict) | Higher operational energy bills | Active, ongoing |

| Business rates relief removed | Significant for larger stores | From April 2026 |

| NLW increase April 2026 | Labour cost rise | Active |

| NI contribution rise | Employer cost rise | Active |

| Plastic packaging tax | ~£2bn sector cost | Active |

| Supply chain costs (Hormuz) | Input cost pressure on imported goods | Ongoing |

The result is a classic margin vice: costs rising on one side, revenue flat or falling on the other. For a mid-market retailer operating on a 10-12% net margin, a simultaneous 3-5% cost rise and a 2-3% revenue decline is not a warning sign. It's an existential event, modelled over a full year.

The UK mid-market retail stall pattern that GrowSights has been tracking for the past 18 months has a new accelerant. Operators who were managing a slow grind now face a fast one.

10. What the World Cup Might (and Might Not) Do

Helen Dickinson and KPMG's Linda Ellett both reached for the same lifeline in their April comments: the football World Cup, scheduled for summer 2026. There is a genuine precedent for major sporting events providing short-term consumer spending uplift -- particularly in electronics (TVs and sound systems), homeware, and food and drink.

The BRC noted early signs of TV and sound system demand picking up in anticipation of the tournament. This is real and shouldn't be dismissed.

But mid-market operators need to be careful about what the World Cup can and cannot do for them.

The categories that benefit are mostly concentrated: electronics retailers, off-licence and grocery, certain home entertainments brands. The World Cup will not revive furniture sales or travel bookings. It will not restore consumer confidence in general discretionary spend. It creates a specific, bounded window of elevated spending in specific categories.

For retailers outside those categories, the risk is actually the reverse: the World Cup may further concentrate consumer discretionary spend into a few weeks, leaving the periods before and after the tournament feeling even flatter. Consumers who have been saving up will spend on the tournament. Then they'll go back to saving.

The GrowSights view is this: plan for a World Cup uplift if you're in the right category to benefit, and don't plan for it if you're not. Don't build a Q3 forecast that assumes a general consumer revival on the back of football. The data doesn't support that read.

📊 Chart: UK GDP growth forecasts revised down following Iran conflict -- IMF April 2026 WEO

11. The Digital Channel Gap Is Widening

One of the quieter signals in the April data is worth pulling out: online non-food sales fell 2.3% in April, but health and beauty moved to first place in BRC's online category rankings. In-store non-food was down 4%. That's a meaningful channel gap.

Consumers who are still spending on discretionary categories are moving more of it online. This is partly convenience and partly price discipline -- online channels make comparison shopping easier, and a consumer watching their outgoings is more likely to search for the best price before committing.

For mid-market retailers with underinvested digital channels, this is a compounding problem. Your in-store foot traffic is declining because consumer confidence is low. Your online channel is not capturing the residual spend because it isn't competitive enough in speed, experience, or price clarity.

The ONS March 2026 retail data showed non-store retailers (predominantly online) at their highest volume level since February 2022. That recovery in online retail happened before April's downturn. If anything, April's data -- with beauty dominating online rankings -- suggests the consumer is using online as the channel of choice precisely when they're being careful.

| Channel | April 2026 non-food performance |

|---|---|

| In-store non-food | -4.0% YoY |

| Online non-food | -2.3% YoY |

| Online health & beauty ranking | 1st (up from 5th in March) |

| Online non-store retailers (March ONS) | Highest since February 2022 |

The SaaS stack tax on retail margin article on GrowSights covers why many mid-market operators are paying for digital infrastructure that isn't translating to digital revenue -- a particular liability now, when online is the channel that matters more.

12. The Honest Diagnosis: Three Things Retailers Get Wrong Right Now

Most retail commentary in a downturn defaults to three bad responses. We see them every time.

Bad response 1: Wait it out. The logic goes: this is a temporary shock, confidence will recover when the war situation clarifies, we'll be fine if we just hold our nerve. The problem is that "temporary" shocks have been arriving every 12-18 months since 2020. Covid. Ukraine. Cost of living. Iran. The consumer has been stress-tested so many times that caution has become their resting state. Waiting for the shock to pass assumes it will. EY's chief economist called the cautious spending pattern "more structural than temporary." Take that seriously.

Bad response 2: Discount your way through it. Revenue needs protecting. Margins need protecting more. A mid-market retailer running a 40% off sale to drive April-May volume is converting a revenue problem into a margin problem and training their customer base to wait for the next discount. It's the worst trade in retail. You can do it once. You can't do it as a strategy.

Bad response 3: Add marketing spend without changing the message. More reach for a message that isn't working is more expensive not-working. The April consumer isn't not buying because they haven't seen your ads. They're not buying because they're anxious about costs and future uncertainty. That anxiety doesn't get resolved by a better Facebook campaign. It gets resolved by specific, honest communication about value, quality, durability, and why this product is worth buying now rather than later.

The right responses look different. They involve knowing your customer's financial situation with more precision than you currently do. They involve building a case for why your product is the right spend, not just a good one. And they involve diversifying your revenue exposure away from the categories most vulnerable to deferral.

That's what retail growth engineering actually means -- it's not a framework for good times. It's the methodology that keeps mid-market operators making decisions off data when the market is telling them to panic.

Caption: Data-led decision-making becomes more critical during spending contractions when every misallocated marketing pound compounds the problem. Source: Unsplash

Caption: Data-led decision-making becomes more critical during spending contractions when every misallocated marketing pound compounds the problem. Source: Unsplash

Key Lessons for Retail Leaders

Lesson 1: External Shocks Don't Create New Consumer Behaviours -- They Accelerate Existing Ones

The Iran war didn't make UK consumers suddenly cautious. It gave permission to a caution that was already forming. PwC's sentiment index had been hovering near zero for months. EY had already flagged that discretionary spending was being structurally redirected before the conflict began. The April drop wasn't a surprise to anyone watching the underlying data closely. It was an inflection point in a pre-existing trend.

The implication is that the recovery, when it comes, also won't be sudden. Structural caution unwinds slowly. Confidence indices take quarters to recover, not weeks.

Ask yourself: Is your planning calendar built around the assumption that things bounce back in H2? Because the data doesn't support that as a base case. What does your business look like if H2 is flat to down?

Lesson 2: Category Is Not Destiny -- But It's More Important Than You Think

Beauty held in April. Furniture stalled. Travel collapsed. These are not random outcomes. They reflect a hierarchy of consumer priority under stress: things that deliver immediate, personal, low-cost reward stay. Things that are expensive, deferrable, and carry future-commitment survive last. Where your category sits in that hierarchy right now isn't fixed -- but changing your position takes longer than a month.

Ask yourself: If your customers were building savings buffers and giving themselves permission to buy one "treat" category, would your product make that list? If you're not certain, that's the answer.

Lesson 3: The Channel You Neglect Becomes the Channel That Fails You

Online non-food held better than in-store in April (-2.3% vs -4.0%). Online beauty went to first place. The direction of consumer behaviour in a cautious market is toward digital, toward price comparison, toward reviews, toward deliberate rather than impulse purchase. Mid-market operators with underinvested online channels are being squeezed at the very moment the channel that matters most is online.

Ask yourself: If a careful consumer who likes your product category went looking for it online today, would they find you before they found a competitor with a stronger digital presence?

Lesson 4: Costs and Revenue Are Moving in Opposite Directions Simultaneously

The April consumer story has almost entirely consumed media coverage. The simultaneous cost shock -- business rates, NI contributions, NLW, energy, supply chain -- has been under-reported. The mid-market operator managing this environment needs to be looking at both sides of the P&L with equal urgency. Revenue protection matters. Margin protection matters just as much, possibly more.

Ask yourself: When you model the next 6 months, are you modelling your cost base accurately -- including the full-year impact of April's business rate change -- and not just your revenue scenario?

Actionable Recommendations

For Retail Business Owners and CEOs

- Build a Q2-Q3 scenario that assumes flat-to-negative consumer spending growth, not recovery. Test your business at 0.3% consumer spending growth (EY's current forecast) and at -1%. Know what each scenario means for your cash position.

- Audit your category exposure by deferability. Rank your product categories from "least deferrable" to "most deferrable" in the current environment. That ranking is your risk register.

- Reassess your promotional strategy. If you're planning discounts to drive volume through a soft period, model the margin impact over a full quarter before you commit. A 20% discount on a 15% margin product isn't revenue protection. It's trading margin for turnover.

- Don't let the World Cup distort your planning. If you're not in electronics, grocery, or directly event-adjacent categories, treat Q3 as a flat environment and plan accordingly.

- Revisit your online channel investment urgently. If in-store non-food is running at -4% YoY and your online channel is underperforming, you have a channel gap that is compounding monthly. This is not a "sort it later" problem.

For B2B Leaders and Suppliers to Retail

- Your retail clients are facing a margin vice simultaneously from costs and revenue. If you're approaching them with price increases -- even justified ones -- expect harder conversations than usual and be prepared to demonstrate value with precision.

- Category data is now a commercial asset, not just a background briefing. If you can bring a retail buyer a credible view of how their category performed in April and where the growth pockets are (health and beauty online, for example), you're useful. If you can't, you're a supplier competing on price alone.

- World Cup planning is already under way for retailers in relevant categories. If you have products or services that play into that window, the conversation should be happening now, not in June.

- Be honest with retail partners about supply chain costs. Retailers know the environment. A transparent conversation about where your costs are going is more credible and more durable than a price rise without context.

For Industry Strategists and Analysts

- The "adjusted" March-April combined figure of +1.5% is the wrong headline. The right headline is that combined growth is below inflation, which means real volumes are still contracting. Be precise about this distinction.

- The IMF's assessment that the UK is more exposed to energy price shocks than its G7 counterparts is structurally important and hasn't received enough retail-specific analysis. The UK's energy cost structure -- including the impact of green levies on industrial energy prices -- means domestic inflation will respond more severely to Hormuz disruption than most other major economies.

- Monitor the World Cup data carefully. If it generates a meaningful consumer spending pulse in late June/July, it will be interesting to see whether that pulse carries through or dies quickly. The answer will tell us a lot about whether the underlying consumer recovery is real or deferred.

Final Summary

| Challenge Category | What Happened | What Your Business Should Do |

|---|---|---|

| Consumer spending decline | First annual fall since Nov 2024; Barclays -0.1%, BRC -3.0% YoY | Build scenarios assuming prolonged softness, not quick recovery |

| Confidence collapse | PwC index fell -12 pts in one quarter; sharpest drop since Ukraine war | Don't wait for confidence to recover -- plan for structural caution |

| Big-ticket freeze | Furniture recovery stalled; travel down 5.7% | Stress-test revenue lines exposed to deferrable, high-AOV purchases |

| Cost pressure compounding | Business rates abolished, NI up, NLW up, energy up simultaneously | Model full-year margin impact of cost changes now, not next quarter |

| Channel divergence | In-store non-food -4%, online -2.3%; beauty leads online | Accelerate digital investment; the cautious consumer shops online |

| Category bifurcation | Beauty holds, fashion soft, big-ticket hit hard | Know your category's deferability score; protect and invest in winning categories |

| Savings shift | Active, deliberate household saving in response to external shock | Marketing messages need to answer "why buy now?" not just "why buy this?" |

| Macro headwinds | UK GDP forecast cut to 0.8%, consumer spending growth forecast at 0.3% | Treat EY's 0.3% consumer spending forecast as your planning base, not a downside scenario |

Grow Your Business With Integrated Data and Operational Intelligence

The April numbers are a signal, not a verdict. But acting on a signal requires seeing it clearly. Mid-market retailers who are flying by instinct right now -- using last year's trading patterns as a proxy for next month's decisions -- are managing a 2026 problem with 2024 tools.

At GrowSights, we work with mid-market UK retail operators to build the data infrastructure and decision-making clarity that makes hard markets navigable. If you want to understand where your business is genuinely exposed in this environment -- which categories, which channels, which customer segments -- and what to do about it, you can start that conversation at growsights.co.uk/how-we-work.

The mid-market operators we work with are the ones who are treating April not as a crisis to survive but as information to act on. That distinction tends to matter a great deal over a full trading year.

Start a conversation with GrowSights.

Research sources:

- Barclays Consumer Spending Report, May 2026 -- via InvestingLive / FashionNetwork

- BRC-KPMG Retail Sales Monitor, May 2026 -- BritBrief, TheIndustry.fashion, FashionNetwork

- PwC Consumer Sentiment Survey Q2 2026 -- BritBrief

- EY UK Economic Outlook May 2026 -- BritBrief, Yahoo Finance, Perspective Media

- House of Commons Library: Economic Update -- Supply Chains and Iran Conflict, April 2026

- ONS Retail Sales: March 2026 -- ons.gov.uk

- GlobalData / Just-Style: UK Consumer Confidence March 2026

- Tokio Marine HCC: UK Retail Sector Report, October 2025

- Energy and Climate Intelligence Unit warnings on food cost projections, 2026

Published by GrowSights | Retail Intelligence and Growth Engineering | Point of View